McGorty Pushes for Pension Reform and Refinance

HARTFORD – State Representative Ben McGorty (R-122) today stood in opposition to Governor Dannel P. Malloy’s pension funding agreement and instead joined with other Republican lawmakers in urging the full legislature to work together to assess alternative methods to address the state’s growing pension system problems.

Republican legislators also released data obtained from two actuarial analyses that show how additional steps can rein in the state’s unfunded pension liabilities. Both reports show how pairing pension finance changes with modifications to state employee benefits could increase the solvency of the state pension plan.

“Today we didn’t see any bold action or needed reform on state employee pensions,” said Rep. McGorty. “Instead, we saw the continuation of the old ways that have gotten us where we are with huge increased costs passed on to future generations – generations that are actually finding it harder to remain in this state due to decreasing economic opportunities. Unless we make meaningful benefit changes and control costs, we are just handing the problem down to future legislatures again.”

The proposed measure narrowly passed the House on a mostly party-line vote of 72-76, and by an 18-17 vote in the State Senate with Lt. Governor Nancy Wyman casting the tie-breaking vote.

Information attached includes:

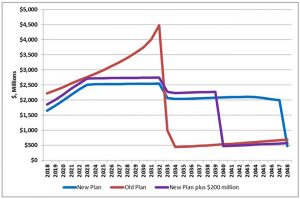

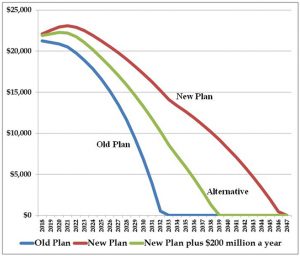

- An analysis from actuaries at the Reason Foundation modeling changes to SERS that could be added to the SEBAC agreement funding policy changes including: adopting a defined contribution retirement plan for new hires, increasing employee pension contributions to 4%, and capping cost of living adjustments to 2% – which would save the state approximately $100 million annually.

- An analysis from actuaries at the nonprofit Pew Charitable Trusts showing the reduction in unfunded liability that could be achieved with $200 million in state employee pension benefit changes. Pew confirmed that if the $200 million is sent back into the fund it would cut 7 years off the length of the refinancing, thereby saving taxpayers billions in future payments.