Latest News

Loading articles...

Loading photos...

State Representative

District

149th

Towns

2

Latest Updates

Swipe through recent posts

.png)

House Republican Leader Vincent Candelora recently announced that State Representative Tina Courpas (R-149) will serve as his appointment to Governor Lamont's Blue-Ribbon Commission on K-12 Education Funding and Accountability. The commission will conduct a comprehensive review of Connecticut's education funding system and issue recommendations to the Governor and General Assembly. Its scope includes the state's current funding landscape, models from other states, the primary cost drivers facing school districts, and proven strategies that have delivered better outcomes for students. The Governor announced the creation of the commission—via executive order—during an April 16 news conference. "Tina has quickly established herself as one of our strongest voices on fiscal policy through her work on the Appropriations Committee, where she has developed a deep understanding of how state funding decisions ripple down to municipalities, taxpayers, and ultimately students," House Republican Leader Candelora (R-North Branford) said. "Her leadership last year on the Select Committee on Special Education gives her valuable perspective on one of the most pressing cost and equity challenges in K-12 education today." Courpas is serving her first term serving the 149th Assembly District, representing residents of Greenwich and Stamford. "I appreciate that Leader Candelora has provided me this opportunity to serve. The commission's work couldn't be more timely. School budgets are escalating, the Education Cost Sharing formula is failing communities across Connecticut, and local property taxpayers are left holding the bill,” Rep. Courpas said. "There is a way we can support robust funding of education in this state without ignoring the very real financial strain on the residents funding these local school systems. I am excited to begin this work and have a meaningful positive impact for both Connecticut students and the taxpayers.”

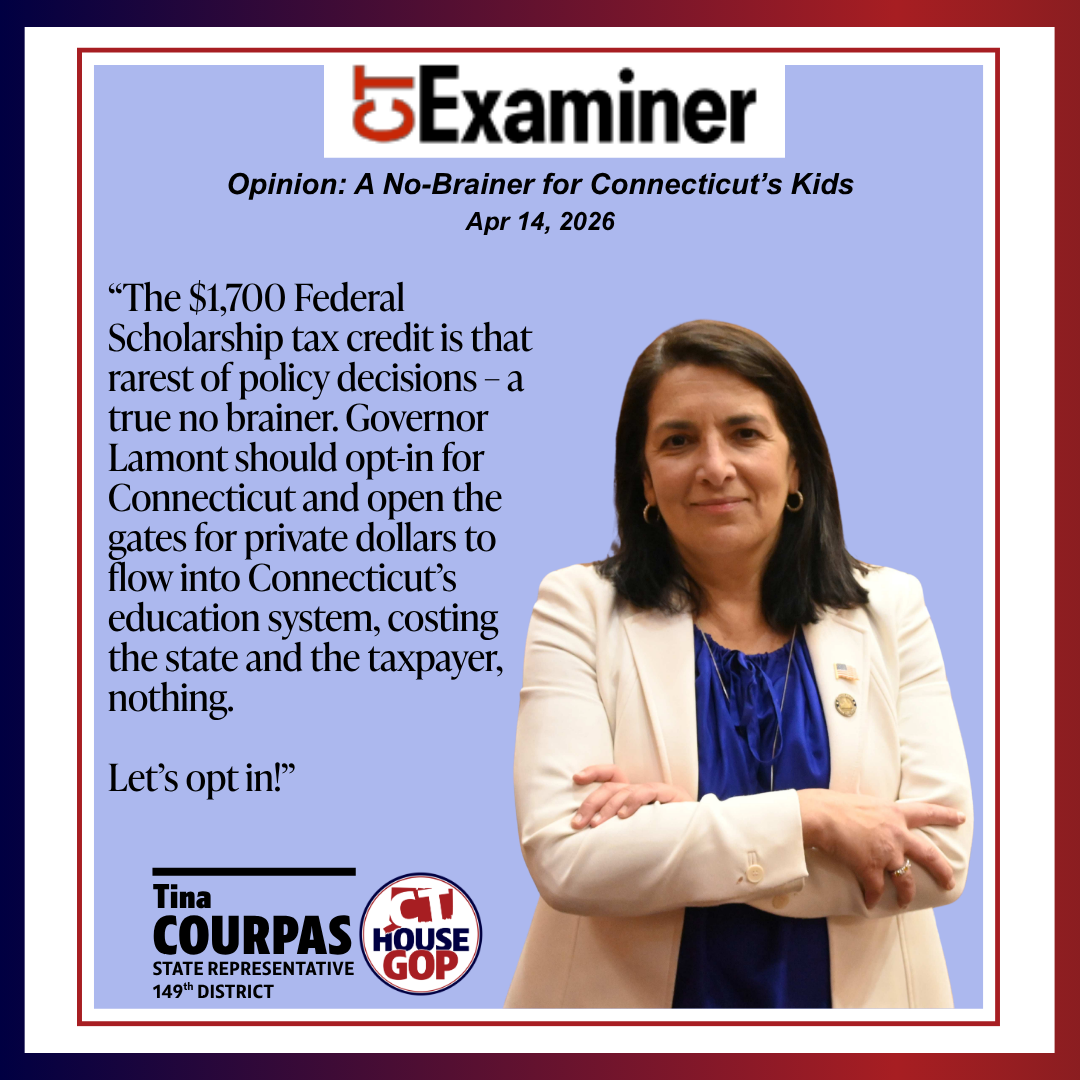

Politics rarely presents “no-brainers,” especially ones on which both sides of the aisle can agree. But, the new $1,700 federal tax credit scholarship law is a true “no-brainer,” a “win-win,” and something CT should adopt as soon as possible. The July 2025 federal law is an opportunity to expand K-12 education for children in public, charter, private and religious schools in every state. Any citizen who makes a charitable donation to a qualified “scholarship granting organization” (SGO) will receive up to a $1,700 dollar-for-dollar federal tax credit. Yes, if you make a $1,700 contribution to an SGO, you get the money right back as a $1,700 deduction off your federal tax bill. In effect, the federal government will pay for your donation, entirely. The uses of the scholarship dollars are broad. The money can be used for tutoring, special needs services, extended day programs, education technology and software, supplies, transportation, tuition, and other expenses listed in the current federal Coverdell Savings Account program. Approximately 90% of CT students are eligible for the scholarships provided by these funds. They cover kids in the most underserved households to kids with household incomes up to 300% of regional median family income. For CT kids to benefit from this law, the Governor must simply elect to “opt-in,” setting up the framework in CT. What does it cost the state of CT? Only the cost of creating the “list” of SGOs. What does it cost the CT taxpayer? Nothing more than that. What does it cost your local school board? Nothing. The program is the federal government’s way of encouraging private donations to education by refunding the money back to donors. Over 23 states have already opted in or expressed their intent to do so, including Virginia (blue), South Carolina (red) and Nevada (purple). This means that If CT doesn’t opt-in, millions of new dollars in CT private donations could go to states that do participate. So, unless the Governor takes action, CT taxpayers will simply make the donations to SGOs in other states; taxpayers here will receive the federal tax benefit, but those scholarships will benefit kids in other states. The $1,700 Federal Scholarship tax credit is that rarest of policy decisions – a true no brainer. Governor Lamont should opt-in for CT and open the gates for private dollars to flow into CT’s education system, costing the state and the taxpayer, nothing. Let’s opt in!

.png)

“CT Public Sector Wage Increases: What About the Taxpayer?” Unfortunately, most of us have been the man in the cartoon. Sometimes we get a raise; sometimes we don’t. Sometimes we even get laid off and our salary disappears completely, at least for a time. Private sector wages don’t generally go up every single year, year after year. That’s why the state of Connecticut can’t afford to continue increasing wages every single year for state employees. I wish we could, but the Legislature is raising public sector wages faster than the taxpayers’ (like the guy above) ability to pay for it. It’s financially unsustainable. And yet, that is what is happening. In the past 6 years, CT state employee wages have risen every year compounding to 33% growth. And this year, the union agreements proposed continue increases through 2029 - for a compound increase of almost 60% over 10 years. CT state employees are already the #2 highest paid in the country. With the raises proposed, CT will be #1. What’s more, state employee wages set pensions. Every time there is a pay raise, state employees’ pensions are higher in perpetuity. Finally, add to this that CT state health benefits are also the #2 most generous in the country for current workers and #1 for retirees. Continuing public sector wages increases for four more years is especially problematic because CT isn’t properly funded to pay the wages and pensions we ‘ve already promised. Our state has the highest debt burden per taxpayer of any state in the country (tied for #1 with NJ), and our pension plan funding ranked #46 out of 50 states. So, how can we get our financial house in better balance? CT should stick the Fiscal Guardrails and continue paying down pension debt (the majority voted to violate them by approx. $2 billion last year). Let’s create a more business-friendly regulatory framework to attract business and increase corporate tax revenue. Finally, let’s freeze CT state employee wages for 2 years. Reports suggest that while public sector wages grew 33% in CT, private sector wages grew 23% over the same time frame. A temporary freeze could give the private sector taxpayer (above) time for his/her wage increases to catch up to the state’s wages for which he/she is responsible. CT public sector wages and benefits are the largest component of our entire budget. I believe that state employee wages should continue to increase – but only if we can answer the question: can the state – i.e., the taxpayer - afford it?

The “dumbing down” of complex policy issues into partisan shorthand attacks is a characteristic of today’s politics that I am working to change. I believe that Connecticut does a better job managing our political landscape than the federal government and certain other states. Speaker of the House Matt Ritter (D-Hartford) and House Minority Leader Vin Candelora (R-Branford) set a civilized tone in the CT House of Representatives, and the dialogue is usually substantive. CT has a lot of which to be proud. And yet, we are not immune. Taking votes on the CT House floor is not easy, even in the best political climate. The issues are often nuanced; one might support parts, but not all of a bill; one might support the purpose of a program wholeheartedly, but the state cannot afford it. Legislators must often balance competing priorities. The problem with today’s politics, even in Connecticut, is that sometimes the substance of these complex policies is distilled down to a one-dimensional cudgel that either party uses to hit the other over the head. Even hot button words in the title of a bill can become political grenades. If a bill title contains the words “Reproductive Rights” and a legislator votes against it, I have seen it used as “proof” that this legislator is not pro-choice, regardless of what the underlying bill says. If a legislator supports a bill with “Gun Control,” that alone can be used as “proof” that such person opposes the Second Amendment. The title words “Trust Act,” “Transgender,” “Women’s Sports,” “Voting Equity,” “Voting Security,” even “Freedom” can all carry political risk - regardless of what the underlying bill says . This sounds like an exaggeration, but sadly, it is not. I heard one House member say to another on the House floor this year: “I can’t vote ‘no’ on this Bill. The title says ‘Elderly.’ If I vote no, next election my opponent will say on a campaign mailer that I hate the elderly.’” At the Special Session in November, I voted against establishing a temporary $500 million “side-fund” created for the Governor to use largely at his discretion. The fund was originally intended to make up for shortfalls in SNAP and other important funding due to the federal government shutdown which had begun on October 1. The “side-fund” would last only until February 4, 2026, until the legislature reconvened and could appropriate funds in the normal budget process. I supported that proposal. However, by the time the bill went to a vote, the shutdown emergency for which the bill was originally created - was over. Yet, the bill proceeded. At the time of the vote, the bill’s proponents could not demonstrate any specific monetary deficit, any program terminating, any quantifiable decrease in SNAP benefits before February 4, which would justify a “side-fund,” departure from our standard budgeting practices. The “side-fund” was also in my view, a clear violation of the fiscal guardrails which I had promised to uphold. I voted no, along with other legislators. I recently read a partisan shorthand attack which obfuscated the issues underlying this vote, calling it simply a vote “against SNAP benefits.” The problems with this dynamic are obvious. Policy involves tradeoffs, and one-liners don’t explain those. Knee-jerk reactivity gets in the way of simply asking questions, getting the facts and understanding the issues. Finally, the dumbing down dynamic is a race to the bottom – who can be angrier, who can make the content of a bill seem more extreme, and who can make the “other side” look worse. So, what is the solution to this “dumbing down” of our state democracy? I welcome your input. I believe that part of the solution is to resist the trend. I am committed to doing that. As a State Representative, I believe this means asking questions, casting votes on the substance, providing full information to the people I serve, and trusting them to digest it. It is a privilege in all respects to represent the 149 th District, including the fact that its citizens care, read, engage, and generally digest the issues at a very high level. Thank you for the privilege of serving you. We should cultivate this ability to look deeper than the latest partisan attack, both in our community and in any and every district in our state, thereby resisting the race to the bottom. If the alternative is the continued “dumbing down” of our democracy, we have no choice but to resist.